Minnesota got high on beer first

The Legislature just passed a 105-page bill that stitches Minnesota's accidental taproom THC market and its brand-new dispensary market under one roof. It's sitting on the governor's desk.

Two days ago, on Sunday May 17, the Minnesota Legislature passed a 105-page cannabis omnibus bill. The House took it 92-42. The Senate repassed it 34-33, which is about as close as a vote gets. As I'm writing this on Tuesday it's sitting on Governor Walz's desk waiting for a signature.

The bill does a lot of things. The one that actually matters, the thing I want to talk about, is buried in the boring parts: Minnesota is finally merging its two cannabis markets into one. And to understand why that's a bigger deal than it sounds, you have to understand that Minnesota built one of the strangest cannabis markets in America, mostly by accident, mostly out of a brewery.

Let me back up.

The slowest fast market in America

Minnesota's official cannabis timeline reads like a state that really, really did not want to be in this business.

Medical cannabis: Governor Dayton signed it in May 2014. Patients couldn't actually buy anything until July 1, 2015. The program launched deliberately tiny, two operators, a short list of qualifying conditions, no smokable flower for years. It was one of the most restrictive medical programs in the country and it stayed that way for a long time.

Adult-use legalization: Governor Walz signed it on May 30, 2023. Minnesota became the 23rd state to legalize.

First legal non-tribal adult-use sale: September 16, 2025. At a Green Goods store in downtown Minneapolis. That's 840 days after Walz signed the bill. Per the Minnesota Reformer that's the fourth-longest rollout of any adult-use program in the country. Two-plus years from "it's legal" to "you can actually buy it from a store that isn't on tribal land."

So that's the official story. Slow medical program in 2015. Legalize in 2023. Stores in late 2025. Eleven years from medical sales to recreational sales, and Minnesota took its sweet time at every single step.

Except that's not actually the story of how Minnesotans started buying THC. Not even close.

The part where a brewery state legalized THC seltzer by accident

Here's the good part.

On July 1, 2022, more than three years before the first dispensary opened, hemp-derived THC edibles and beverages became legal in Minnesota. Up to 5mg of THC per serving, 50mg per package. The chemistry of that THC is identical to the THC in a dispensary gummy. The molecule does not care which plant it came from or which bill made it legal.

The wild part is how it happened. It passed the Republican-controlled Senate unanimously. Zero debate. The legislators who voted for it have said, on the record to NPR, that they didn't fully realize what they'd done. The bill's author called it a "technical fix" that "winded up having a broader impact than I expected." NPR ran the headline "Minnesota legalized THC edibles and infused drinks ... by accident?" Vice went with "Oops, Minnesota Accidentally Legalized THC-Spiked Seltzer." That is a real thing that happened to an entire US state.

And here's why Minnesota specifically was the perfect petri dish for this: Minnesota is a beer state. Surly, Indeed, Bauhaus, Modist, Fair State, Fulton, a genuinely deep craft brewing culture and the taprooms, distributors, and liquor stores that come with it. So when 5mg THC seltzers became legal, the beer industry didn't have to invent a market. It already had the cans, the distribution, the taprooms, the liquor-store shelves, and the customers. Indeed Brewing put out Two Good. Modist put out TINT. Bauhaus put THC seltzer in its taproom. The hemp-THC drink didn't sneak into Minnesota through head shops. It walked in through the front door of the craft beer industry.

So picture the actual timeline from a normal Minnesotan's point of view. By summer 2022 you could buy a low-dose THC seltzer at the liquor store down the street, or crack one at a taproom. By fall 2025, three-plus years later, the first dispensary finally opened. For most of the state, for most of that window, the de facto adult-use cannabis market WAS hemp THC drinks sold next to the IPAs. Slow, beer-loving Minnesota accidentally built the most interesting two-track cannabis market in the country and then spent three years not noticing.

What the actual regulated market looks like now

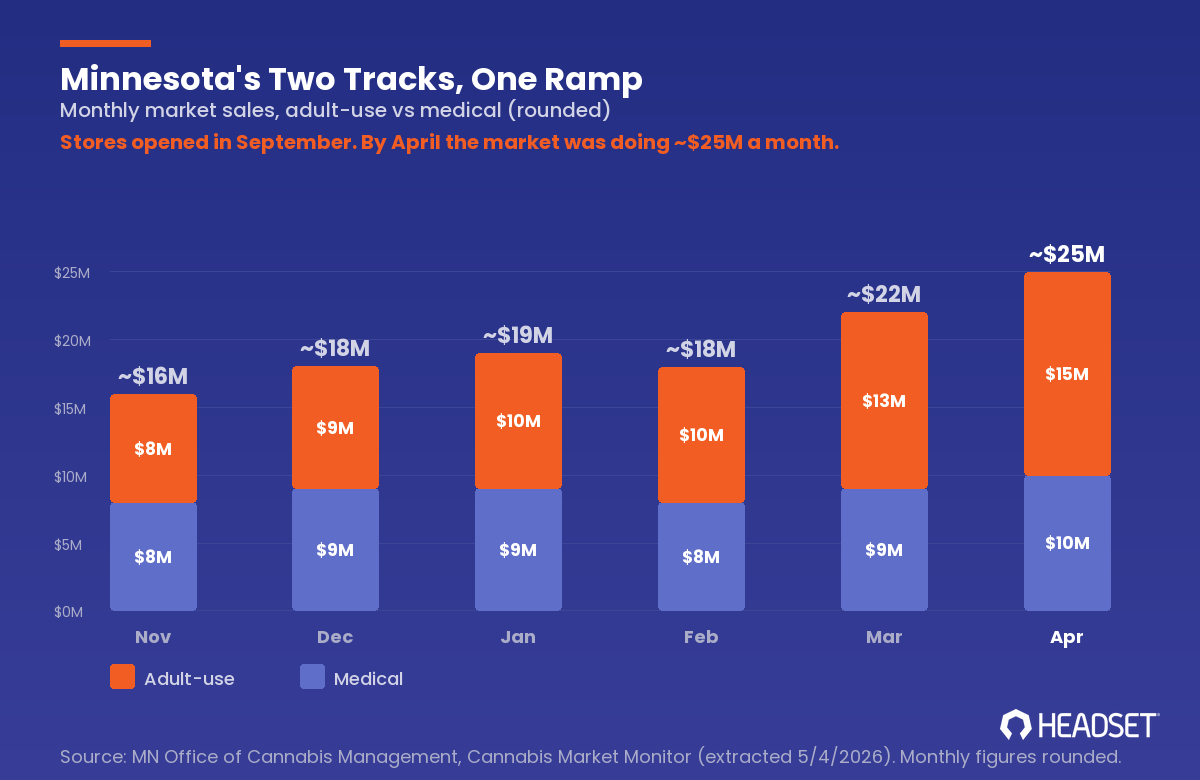

The dispensary side is young, it opened in September, but the early numbers from the Minnesota Office of Cannabis Management's Cannabis Market Monitor (data extracted May 4) tell a clear story.

Trailing-twelve-months: $177.85M in market sales across 2,085,076 transactions.

The monthly ramp is steep. Rounding the OCM figures:

November: ~$16M

December: ~$18M

January: ~$19M

February: ~$18M

March: ~$22M

April: ~$25M

Look at the split inside those bars. Medical and adult-use started basically tied (about $8M each in November). By April, adult-use was ~$15M and medical was ~$10M. The recreational side is accelerating noticeably faster than medical, which is exactly what you'd expect, except in Minnesota the medical program had a 10-year head start AND, for those first months, the supply chains were legally walled off from each other.

That walled-off supply chain is the thing the new bill blows up, so hold that thought.

Then there's the price story, which is genuinely backwards.

Per OCM, trailing-twelve-months median price per gram of flower: medical $9.52, adult-use $14.54. Adult-use flower costs 53% more than medical flower in Minnesota.

In a mature market this is upside down. Go look at almost any market that's been running adult-use for years and medical flower trades at a premium or close to parity, because medical patients buy higher-potency, often higher-cost product and the rec market has been beaten down by competition and oversupply. Minnesota is doing the opposite, because the rec market is three months old, supply is tight, there's no price war yet, and the medical program has a decade of operators who already figured out their cost structure. Minnesota's rec market hasn't had its price collapse yet. Every other state's did. It's coming, it just hasn't started.

On volume: medical still moves more flower (128K oz, 54%) than adult-use (108K oz, 46%) over the trailing year, but adult-use is closing that gap fast given it's only been selling since September.

Category mix, also from OCM, shows the market maturing in fast-forward. Share of annual sales by product type:

2023: Flower 43.9%, Concentrate 29.6%, Edible 9.6%, Shake/Trim 5.8%, Nonedible 11.0%

2025: Flower 48.1%, Concentrate 29.3%, Edible 8.8%, Shake/Trim 9.7%, Nonedible 4.1%

2026 so far: Flower 47.2%, Concentrate 33.2%, Edible 7.6%, Shake/Trim 11.7%

Concentrate climbing toward a third of the market while edibles and nonedibles compress. That's a market growing up quickly. (And note: the licensed-store edible number is being quietly held down by the fact that for years the edible buyer in Minnesota was already served by the hemp-THC channel at the liquor store. The two markets have been competing the whole time. They just weren't allowed to admit it.)

One more structural quirk worth knowing: Minnesota runs a dual supply chain. Product gets designated adult-use or medical all the way back at cultivation. That is the specific thing the new bill is about to change.

The seven changes, and the one that matters

The omnibus bill (HF4203 / SF4401) is the thing the Star Tribune broke down into seven changes. Here they are, with what I actually think about each:

Party-size hemp beverages, August 1. Hemp retailers can sell THC drinks in big child-resistant, resealable bottles, 750ml or more, 17+ servings. Translation: the THC growler. Minnesota inventing the cannabis equivalent of a box of wine for your cabin weekend is the most Minnesota sentence in this whole piece.

"Ratio" hemp-infused products, January 1. You'll be able to buy THC + CBD/CBG/CBN/CBC blends outside the medical market, up to 10mg THC per serving (200mg per edible package). This is a real product expansion for the hemp channel, not a footnote.

Merged medical and recreational supply chains. This is the one. More below.

Macrobusiness license, January 1, 2027. A bigger license tier: large indoor canopy, up to eight retail stores, with a chunk required in "high medical need" areas OCM designates. It replaces the old medical combination business and effectively reshapes who the big operators are.

Expungement cleanup. If you were convicted on a cannabis count in a multi-charge case and the other counts were cannabis-related and dismissed, the whole thing gets sealed. Modest, good, overdue.

The tax goes from 10% to 15%. The gross receipts tax rises and local cannabis aid gets repealed (this comes out of the 2025 tax agreement). Minnesota's effective cannabis tax was already not low. Operators should be modeling this now.

Delivery-only option for lower-potency hemp edibles. The gummies and the seltzers can be delivery-only operations. The taproom-and-liquor-store market gets a doordash lane.

Six of these are normal cannabis-bill housekeeping. Number three is the whole ballgame.

Why merging the supply chains is the actual story

Right now, as I covered above, Minnesota designates product as medical or adult-use all the way back at cultivation. Two parallel pipelines. Separate inventory, separate tracking, separate everything, from the plant to the shelf. It is expensive and it is dumb, because it's the same plant.

The bill collapses that. Under the new framework the medical and adult-use supply chains merge. The only place the distinction survives is at the point of sale: a registered medical patient gets product marked with a sticker and sold tax-free. Behind the counter, in the grow, in the warehouse, in the tracking system, it's one stream. (The detailed version phases the heavier operational pieces in over time to give operators room to transition, but the direction is set.)

Here's why I care about this more than the THC growler.

For an operator, a forked supply chain is a tax on existing twice. You're running two inventories, two compliance regimes, two sets of COGS, two of everything, to serve a medical registry that in most maturing markets shrinks every year once rec is available. Minnesota built a fence down the middle of every operator's warehouse and then is now, three months into rec sales, tearing the fence down. That's the right call. It frees up working capital, simplifies the tech stack, and lets the medical program survive as a patient-benefit layer (tax-free, sticker, priority service) instead of a parallel universe nobody can afford to keep staffing.

And it does something bigger. It pulls Minnesota's three cannabis worlds, the old medical program, the new dispensary market, and the accidental beer-aisle hemp-THC market, under one regulator's roof. The Office of Cannabis Management is the body that's supposed to hold all of this. Medical, adult-use, and lower-potency hemp edibles, governed together instead of as three feuding silos that pretend they don't compete. Minnesota's two-track market becoming one track, on purpose, is the entire arc of this state's weird cannabis history finally resolving into a sentence that makes sense.

The federal piece makes the timing sharper. The federal hemp definition tightens on November 12, 2026 (total-THC standard, a tiny per-container cap, synthetics out). A huge slice of today's hemp-THC products, the 5mg seltzers very much included, don't survive that cap as currently sold. Minnesota's hemp-THC market is real money. So the smart read of this bill isn't just "merge the weed pipelines." It's Minnesota building the on-ramp for its beer-aisle THC operators to transition into the licensed cannabis system before the federal floor drops out from under them. The merge isn't only tidying up. It's a bridge built right before the old road washes out.

What I actually think

Minnesota did this backwards and somehow that's the interesting part.

Most states legalize, stand up dispensaries, and then spend years fighting the hemp-THC gray market that pops up alongside. Minnesota got the gray market first, by accident, through its breweries, and let it run as the de facto adult-use market for three years while the official program crawled. Now it's legalizing the dispensaries, merging the supply chains, and pulling the hemp channel under the same regulator, all roughly at once, right as the federal hemp rules tighten.

If you operate anywhere, here's the transferable lesson, and it's not a small one: the hemp-derived THC market is not a sideshow you can regulate later. In Minnesota it was the market for three years. Every state still pretending the gas-station and liquor-store THC channel is separate from "real" cannabis is making the mistake Minnesota already accidentally ran the experiment on. The states that win the next five years are the ones that figure out, on purpose, what Minnesota figured out by tripping over it: it's all one market. The plant doesn't care. The customer doesn't care. Eventually the regulator stops pretending to care, and the smart operators are positioned for the day it merges.

Walz still has to sign it. Assuming he does, I'll be watching the medical share. If a merged supply chain plus a tax-free sticker keeps Minnesota's medical program meaningfully alive instead of letting it wither the way it has almost everywhere else, that's a model worth copying. If it withers anyway, that tells you something too.

Either way: slow, beer-loving Minnesota built one of the most instructive cannabis markets in the country, and it did it mostly by accident, mostly out of a taproom. I did not have that on my 2026 card. I'm glad it's there.

See you next week.

— Cy

“Well, at least we got that right” - she says from MN 😂